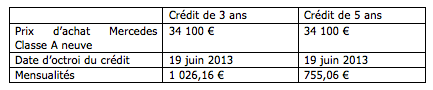

Are you considering making a purchase that exceeds your monthly financial means and savings? One thing is clear: you will turn to the credit market.

Are you considering making a purchase that exceeds your monthly financial means and savings? One thing is clear: you will turn to the credit market.

Will you go to a traditional bank or a specialized credit broker?

Two solutions offering different services.

At first glance, nothing too difficult

Except that since 2012, the economic situation is different. The financial crisis linked to the public deficit of European countries has left its mark and austerity policies implemented by governments have an undeniable impact on the credit market. Indeed, banking activity is now under scrutiny and in this area, one word reigns supreme: caution.

The figures speak for themselves: the number of mortgage loans contracted in Belgium decreased by 23% in March, compared to March 2011. In France, over the same period, the drop is staggering: -47%. The number of credit applications in Belgium fell by 20%. The amount of loans granted also recorded a smaller decrease of 9%. The amount for credit applications contracted by 5% (Le Soir Online, “Decrease in mortgage loans in March”, Thursday, April 12, 2012).

Consequence?

New customers of Crédit Populaire Européen have already noticed. It is becoming very complicated to obtain credit from your usual banker. Banks are becoming increasingly demanding. With this worrying consequence, the number of bankruptcies in Belgium increased by 26% in the first quarter of 2012.

It would therefore not be surprising for consumers who are used to dealing with their usual banker to turn to independent credit brokers to check the conditions of access to credit and the financial terms offered to them.

Independent credit brokers are, unlike banks, credit specialists. Their professional activity is almost exclusively based on granting credit. This is not the case for a bank, which largely depends on investments made with their clients’ savings. In other words, access to credit is therefore much easier with an independent broker.

Traditional bankers are an essential link in economic policy, and today more than ever, they are key players. They are monitored by the Banking and Finance Commission, the National Bank of Belgium, and the government, which legitimately wishes to avoid fiascos like the near-bankruptcies of Fortis and Dexia banks. Consequence? The measures taken by banks are sometimes more “media-driven” than economic. An independent broker enjoys greater flexibility. They accept or reject your file based on objective financial elements rather than a general policy that no longer makes distinctions.

Finally, and it is obvious, your usual banker can only offer you “in-house” products and cannot benefit from the enormous diversity of other products available on the market. An independent broker works with many different financial partners.

At Crédit Populaire Européen, we have over 20 financial partners who will have a different perspective on your application. An independent broker is therefore much more able to take advantage of the competition among financial partners.